week three- budgeting

Welcome to our 8 week challenge, where we look to equip you with all the tools you need to take control of your financial future.

Thank you for joining us. We hope there were parts of the session that you found of value.

Further to our session, we wanted to provide useful information to support you in implementing some of the models we discovered.

In particular, how to set your personal financial goals.

Why is a budget important?

86% of Australians have no idea what their monthly expenses are.

The most common reason? “too hard to calculate the expenditure”

Living without a budget may seem like a pretty laid back approach to money, but 59% of Australians without an awareness of their expenses admitted their current financial situation causes them to lose sleep.

how to budget & save

Calculate your monthly take home pay

List your expenses

Split into fixed & variable expenses

Find a budget that suits you

Track your budget

Review your budget

Different Budgeting Methods

The mere mention of the B word can be enough to make some people cringe. But there are a few budgeting techniques you can try:

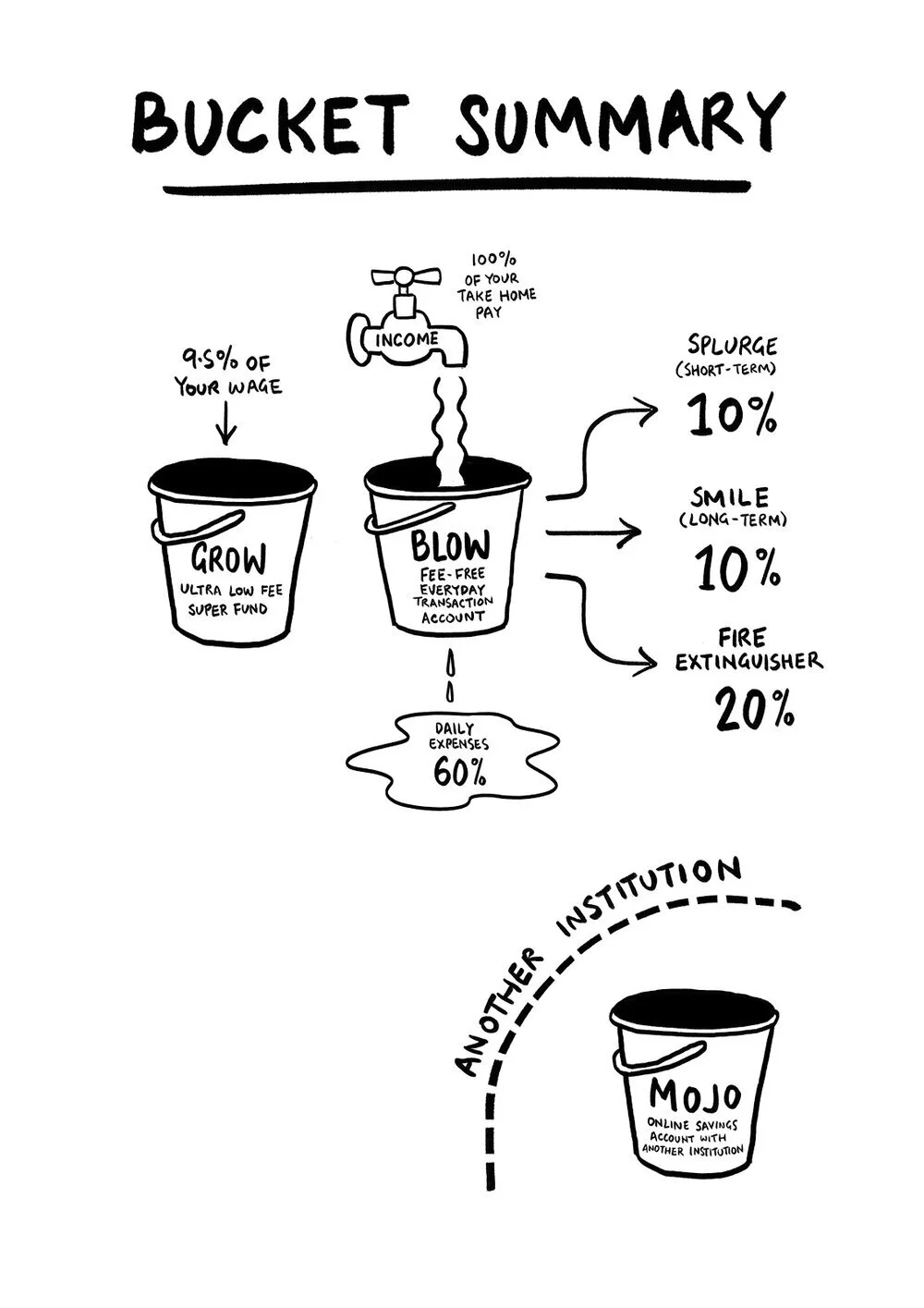

The ‘buckets’ or ‘percentage’ method

If you’ve ever read The Barefoot Investor (or any number of other finance books), you’ll have heard of this method.

In The Barefoot Investor, author Scott Pape suggests the following percentage splits:

60% to your ‘Blow Bucket’ – which is for everyday expenses like your rent, home loan repayments, utilities and food.

10% to your ‘Splurge Bucket’ – which is for things that make you feel good, like socialising or buying new clothes.

10% to your ‘Smile Bucket’ – which is used for savings for fun, longer-term goals like a holiday.

20% to your ‘Fire Extinguisher Bucket’ – which is also for your long-term savings goals, but the less fun ones (house deposit, debt, paying off your mortgage quicker).

The ’50/30/20′ method

This method is basically a simplified version of the buckets method above. The split, in this case, is that you spend 50% of your income on your needs and necessities, 20% on savings or debt payments, and 30% on wants like entertainment, eating out, shopping and travel.

Obviously, the method is pretty much the same in both cases, it’s just a matter of working out what percentage splits will work for you.

Pay yourself first

OR should we say ...make a decision to achieve your goals first.

Even before you pay your bills… it sounds crazy right?

Us humans are completely irrational & very emotional that do things that are not aligned to our best interests.

As discussed, we understand our money-story & money mindset, we have built out our goals.

Now it is about putting structure and framework around this to ensure you can achieve your goals.

This includes putting a budget together.

By paying yourself first, you are taking care of your future and your goals.

The biggest goal with this method is saving. Instead of setting up categories that cover all your expenses, you focus on an ambitious savings goal.

For example, you choose to save 30% of your income. This is immediately deposited into a high-interest savings account. The leftover funds can be allocated wherever you please. Obviously, this method would work if you’ve got a specific savings goal in mind, like a house deposit. But it does leave you at risk of overspending the rest of your income and then falling short if a bill comes up.

The zero-based budget

This budgeting method is great if you’re a meticulous planner who likes to know where every single dollar goes. If you’re not, you’ll probably find this method way too full on.

Essentially, you take your monthly income and give a job to every single dollar. So a certain amount goes towards food, another amount is your rent payments for that month, another portion goes towards saving up for a house deposit – until there is nothing left. Every single dollar is accounted for. This method allows you to be completely in control of your money – but as I’m sure you can imagine, it would be quite time consuming to keep track of where every single cent of your money goes.

Create your own

If none of the methods above have tickled your fancy (and there are plenty of other budgeting styles out there that I haven’t mentioned in this article), you can create your own by using a combination of any of the above.

When it comes to budgeting, the trick is to make it as easy as possible for yourself, otherwise you won’t bother doing it. Find a system that will work for you.

Without commitment, you will never start.

Without consistency you will never finish.

Denzel Washington.

Automate your savings

Once you’ve chosen a savings account, you can set up regular deposits from your salary into your savings account/s.

Choose how often you want to deposit the money and the amount that fits your income (and budget!), and make it automatic. That way, you don’t need to remember to do it manually every week. You can even ask your employer to automatically direct a portion of your fortnightly or monthly income into your savings. By automating your savings, you never actually see the money, so you won’t be tempted to buy things you don’t need. You also won’t sabotage your own efforts by ‘forgetting’ to transfer the money.

Out of sight, out of mind!

Be disciplined

If you find the thought of withdrawing money from your savings too tempting, you could make the funds harder to access by locking them away in a term deposit or a savings account that will penalise you for making withdrawals.

Automating your savings is all well and good, but if you’re regularly withdrawing all your savings for a bit of extra spending money, you may as well not even bother. Doing this completely defeats the purpose of, well, saving. It’s okay to dip into your savings every now and then when money is tight, but don’t make a habit out of it.

Anyone can make a budget and automate money into their savings. But if that’s all it took to be good with your money, financial planners would be out of a job. Being financially disciplined is essential to the success of your savings plan, and being good with money in general.

The Wealth Creation Process - 10 Steps

Goals - what do you want to achieve, what drives you, what gets you out of bed every morning? (Pay down debt, invest, rough timeframe)

Budget - complete your budget spreadsheet as accurately as possible, account for EVERYTHING!

Analyse - Analyse your budget to break expenses into Necessity (can’t live without) and luxury (could survive without)

Value - look for Necessity costs that you may be able to get a better deal on and cut down the cost eg. mortgage, phone bills, food bills etc.

Cut - identify luxury costs that may be detrimental to your success identify those that you may need to cut or decrease to continue to success eg. if your total expenses are over 60% than you need to cut some luxuries.

Percentages - identify what percentage of your income you are currently operating at and get a close to the goal of 60% expenses 40% savings as quickly as possible.

Timeframe - use the percentages and numbers above to re-calculate realistic time frames on your goals.

Structure - use the bucket strategy to set up your accounts to automate where you money goes once you receive it according to your percentages which have been worked out in one of the steps above.

Stress test - run some different good and bad scenarios to see if your budget has enough flexibility to withstand changes and still succeed.

Implement - set up your bank accounts and organise your direct debits etc. to make your budget as automated as possible to be more successful.

Should you have any questions, please do not hesitate to contact us via email info@newcastleadvisor.com

sign up to our wealth portal